�������: 1-15 ���鵽������ѧ bond����ؼ�¼28�� . ��ѯʱ��(0.109 ��)

����ũҵ��ѧCC bond���ٻ����ʡ�����조���ű���MPAccѧ�������������Ƚ���ͼ��

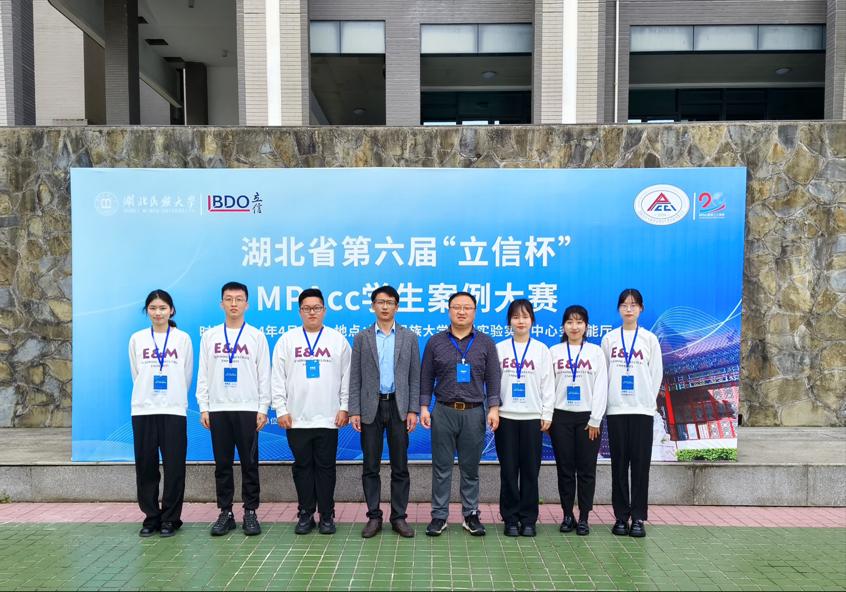

CC bond�� ����ʡ ���ű� MPAcc ���

2024/4/29

2024��4��20-21�գ�����ʡ�����조���ű���MPAccѧ�����������ں��������ѧ�ٰ졣���������ȫ�����רҵѧλ�о�������ָ��ίԱ��ָ��������ʡ���˶ʿרҵѧλ�������죬���������ѧ�а죬�人��ͨ�����Ƽ�����˾�����Ż��ʦ��������������ͨ�ϻ��������Э�졣�������ҽ��𣬻���ũҵ��ѧCC bond��ƾ�����ɫ�����ٻ����Ƚ���

�������±���ѧEric Bond��������ƾ���ѧ���ʾ�����ó��ѧԺ��ͼ��

�������±���ѧ Eric Bond ����ƾ���ѧ���ʾ�����ó��ѧԺ ��ҵ˰�ĸ� ����Ͷ��

2018/6/4

2018��5��9�����磬�������±���ѧ����ϵEric Bond����Ӧ�����ʹ��ʾ�����ó��ѧԺ����ΪѧԺʦ��������Ϊ��Border adjusted taxes, cash flow taxes, and transfer pricing����ѧ�����档���ʾ�����ó��ѧԺ20��λʦ���μӽ�����2016����������������ҵ˰�ĸ�Ĺ������������Ծ���ѧ��������������ۡ�Bond���ڹ����������������ֲ�Ʒ��...

Discussion of "The Cross Section and Time Series of Stock and Bond Returns" by Koijen, Lustig & Van Nieuwerburgh

Cross Section Stock and Bond Returns

2015/7/23

A�� ne model in which:

ñ 3 priced factors explain the cross section of bond and stock returns:

level, CP, DP

ñ 2 factors explain the time variation in bond and stock returns:

CP, DP

Discussion of ��The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks�� by Glenn Rudebusch & Eric Swanson

DSGE Model Bond Premium

2015/7/23

contribution to monetary DSGE literature

⇒

Epstein Zin utility with high risk aversion (improves asset pricing)

can still match volatility of macro aggregates

same spirit as Tallarini (2000,...

From a macroeconomic perspective, the shortterm interest rate is a policy instrument under

the direct control of the central bank, which

adjusts the rate to achieve its economic stabilzation goals. ...

Bond yields respond to policy decisions by the Federal Reserve and

vice versa. To learn about these responses, I model a high-frequency

policy rule based on yield curve information and an arbitrage-...

�人������ѧ��������ѧӢ�Ŀμ�Chapter5 Bonds,Bond Prices and the Determination of Interest Rates

�人������ѧ ��������ѧ Ӣ�� �μ� Chapter5 Bonds,Bond Prices and the Determination of Interest Rates

2015/6/4

�人������ѧ��������ѧӢ�Ŀμ�Chapter5 Bonds,Bond Prices and the Determination of Interest Rates��

The Maturity of Debt Issues and Predictable Variation in Bond Returns

Borrowing and Debt Bonds Investment Return Financial Markets Forecasting and Prediction

2015/5/13

The maturity of new debt issues predicts excess bond returns. When the share of long term debt issues in total debt issues is high, future excess bond returns are low. This predictive power comes in t...

Monetary Policy Drivers of Bond and Equity Risks

Risk and Uncertainty Bonds Central Banking System Shocks Policy Macroeconomics

2015/4/28

The exposure of U.S. Treasury bonds to the stock market has moved considerably over time. While it was slightly positive on average in the period 1960�C2011, it was unusually high in the 1980s and nega...

Monetary Policy Drivers of Bond and Equity Risks

Risk and Uncertainty Bonds Central Banking System Shocks Policy Macroeconomics

2015/4/27

The exposure of U.S. Treasury bonds to the stock market has moved considerably over time. While it was slightly positive on average in the period 1960�C2011, it was unusually high in the 1980s and nega...

Reaching for Yield in the Bond Market

Fixed Income Reaching For Yield Financial Intermediation Insurance Companies Insurance Bonds

2015/4/27

Reaching-for-yield��the propensity to buy riskier assets in order to achieve higher yields��is believed to be an important factor contributing to the credit cycle. This paper analyses this phenomenon in...

Can Civil Law Countries Get Good Institutions?Creditor Rights and Bond Markets in Brazil,1850-2003

Civil Law Countries Creditor Rights Bond Markets

2015/4/20

Can we assume that the effect of early institutions is persistent over time? Work by La Porta,Lopez de Silanes, Shleifer, and Vishny, also known as the ��law and finance�� literature, implicitly argues ...

A CB (corporate bond) pricing probabilities and recovery rates model for deriving default probabilities and recovery rates

Government Bond (GB) model Corporate Bond (CB) model Term Structure of Default Probabilities (TSDP) Recovery Rate (RR) Credit Default Swap (CDS) business portfolio, credit risk management

2012/9/14

In this paper we formulate a corporate bond (CB) pricing model for deriving the term structure of default probabilities (TSDP) and the recov-ery rate (RR) for each pair of industry factor and credit r...

Interest Rate Risk of Bond Prices on Macedonian Stock Exchange - Empirical Test of the Duration, Modified Duration and Convexity and Bonds Valuation

Treasury Bonds risk-free valuation intrinsic value duration, convexity

2012/9/14

This article presents valuation of Treasury Bonds (T-Bonds) on Macedonian Stock Exchange (MSE) and empirical test of duration, modified duration and convexity of the T-bonds at MSE in order to determi...

Binomial Tree Model for Convertible Bond Pricing within Equity to Credit Risk Framework

Binomial Tree Model Bond Pricing Credit Risk

2012/9/14

In the present paper we fill an essential gap in the Convertible Bonds pricing world by deriving a Binary Tree based model for valuation subject to credit risk. This model belongs to the framework kno...

�й��о����������а�-��

- ���ڼ���...

�й�ѧ���ڿ����а�-��

- ���ڼ���...

�����ѧ���л������а�-��

- ���ڼ���...

�й���ѧ���а�-��

- ���ڼ���...

�ˡ���-ƪ

- ���ڼ���...

�Ρ���-ƪ

- ���ڼ���...

��������-ƪ

- ���ڼ���...

�������� -ƪ

- ���ڼ���...

֪ʶҪ��-ƪ

- ���ڼ���...

���ʶ�̬-ƪ

- ���ڼ���...

��������-ƪ

- ���ڼ���...

ѧ��ָ��-ƪ

- ���ڼ���...

ѧ��վ��-ƪ

- ���ڼ���...